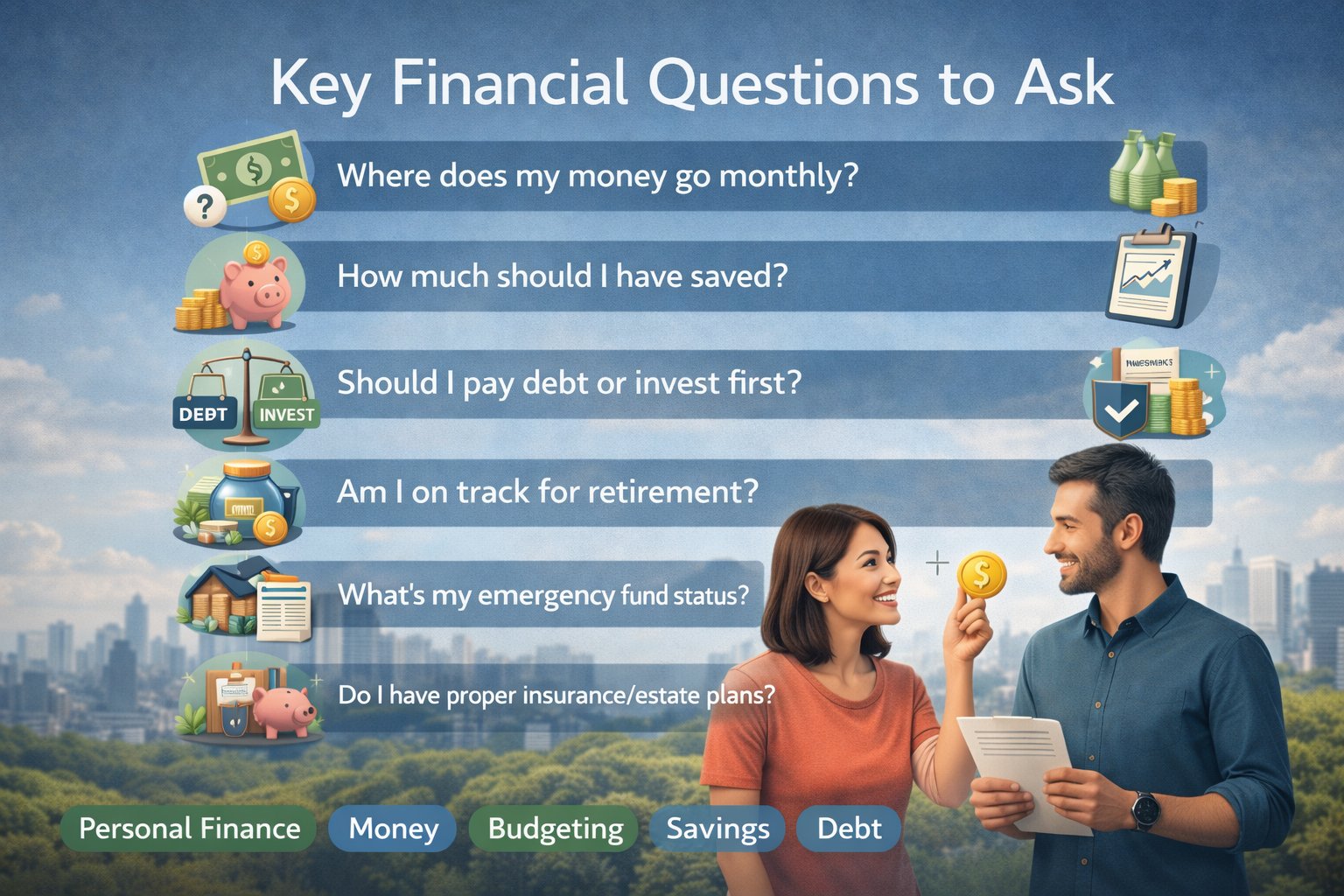

The Most Important Financial Questions

We should ask the following top financial questions (and why they’re important).

It’s not about getting rich, it’s about knowing, acting and getting ready. The most urgent financial issues don’t mean bad luck; they mean not asking the right questions in the early days.

When you’re looking for clarity, control, and confidence with the finance issue, you will want to take this journey. These questions are the best kinds of financial questions that you can ask yourself — but they need to come in multiple flavors, and a lot of time should be spent discussing why they matter and what to do next.

“Where Does My Money Go Every Month?”. This is the bedrock of ALL personal finance.

Why this question matters. You can’t change what you don’t reflect back. It is common for folks to make decent-paying living, to be broke because they don’t have:

How much they actually spend. What is a necessary expense vs an optional expense. Where money is leaking quietly.

What to review. Just take a minute and pose yourself a question. What is your aspiration age of fulfilling and attaining your objective of retiring? What sort of life are you expecting to live when you attain it?

Transportation. Subscriptions. Also, do not forget to include your amount allocated for your debts. Savings and investments. Discretionary spending.

Action step. Follow at least a 30 to 90 day record of expenses with the aid of:

A spreadsheet. A budgeting app. Bank statements.

Objective: Get your head around where every dollar goes.

“How Much Should I Have Saved?”. Savings serve as your shock absorbers when facing financial shocks. Without it, every unanticipated expense becomes a crisis.

General saving benchmarks. Of course, individual progress is necessarily all different, so the following should be taken as a rough guideline, characterised by having: An emergency fund big enough to cover 3-6 months of essential bills. Short-term savings for things such as a vacation, etc. Long-term savings for things such as retirement, etc.

It must be pointed out here that this situation is difficult to manage for many.

No clear target. Saving “what’s left” instead of saving first. Confusing savings with investments.

Action step. Set particular savings goals:

Target emergency fund amount (exact amount).

Monthly savings percent (10-20% if you can reach it).

Have separate accounts for different purposes.

Aim: To make saving a system, not just an option.

“Should I Invest First or Pay Off Debt?”. This is one of the most familiar — and confusing — financial questions.

The real answer: it depends. Key factors include:

Interest rates on your debt.

Debt type (credit card vs student loan).

Employer retirement matches.

Risk tolerance.

General rule of thumb. Higher interest debt (6% – 7%+): focus on payoff. Lower interest debt: balance payoff with investment. Employer match: Nearly always invest enough to get the full match.

Why this question is critical. Debt quietly siphons off future income through interest, whereas investing creates future wealth.

Action step. List all debts with:

Balance. Interest rate. Minimum payment.

Then compare interest rates with realistic investment returns.

Goal: Use money in the most efficient way possible.

“Am I Getting Ready for Retirement?”. Retirement planning isn’t a question of age, of course—it is more about time and consistency.

Why this question is often avoided. Feels overwhelming. Future feels far away. Numbers seem intimidating. However, to ignore it is more costly.

Here are just a few general checkpoints for consideration in retirement savings.

By 30, it’s often suggested that you have your annual income saved, or about one time. By 40, that number is usually about three times your annual income. At 50, you could be shooting for about six times your yearly income. At 60, a common target is between eight to ten times your annual income. Just keep in mind these aren’t strict rules, but more like helpful guidelines.

Action step. What to ask yourself

When do I Want to Retire at What Age?

What kind of lifestyle do I desire?

Am I putting into retirement accounts regularly?

Use retirement calculators to model all possible futures.

Goal: Replace uncertainty with visibility.

“What’s My Emergency Fund Status?”. An emergency fund is not a luxury in itself — it’s protection against life.

What counts as an emergency.

Job loss.

Medical expenses.

Urgent home or car repairs.

Family emergencies.

What it should NOT be used for.

Vacations.

Sales or impulse buys.

Planned expenses.

Common mistake. People often think an emergency fund is too fundamental or boring — until they need it.

Action step. Keep emergency funds:

Easily accessible.

In a high-yield savings account.

Separate from day-to-day spending accounts.

Objective: Stay out of debt when life surprises you.

“Do I Have Proper Insurance and Estate Plans?”. This is the question that will save all you have constructed.

Insurance you should review.

Health insurance.

Auto insurance.

Home or renter’s insurance.

Life insurance (if others depend on your income).

Disability insurance.

Estate planning basics. Even without money, though, you might require:

A will.

Beneficiary designations.

Power of attorney.

Healthcare directives.

Why this matters. Without planning:

Your family can become embroiled in legal complications.

Assets may not get to where you prefer.

Close family members might face financial hardship.

Action step. Develop a habit where you always examine your insurance plans and policies every one year, and always make changes in your policies after a big change occurs in your life.

Besides, don’t forget, the true purpose of all this is to protect the people you care most about, not necessarily the money.

Bonus Questions That Keep Stability From Stress. All these questions deepen financial awareness:

Can I survive 3 months without income?

How much of my income is fixed vs flexible?

Are my financial goals written down?

What financial habits hurt me most?

Am I improving year over year?

How Many Times You Should…..

Try checking in monthly on your spending and cash flow.

Every quarter, review how your savings and debt reduction progress is going.

And then a thorough review of your plans once a year in retirement, insurance, and estates. Of course, review everything since the last big change occurred in your life, such as your marriage, having kids, a new job, or a new living situation.

Final Thoughts: More clarity means more financial excellence. You don’t have to have business knowledge or financial expertise. You just have to ask better questions, consistently.

These do not judge you—they help you understand. The moment you recognize where you feel comfortable with your economic standing, you then have the ability to turn and change course; you can make wiser, deeper decisions that help make the right choices and build long-term economic stability.

Get one question first today. Then build from there.

Share this content:

Post Comment

You must be logged in to post a comment.